Job worries weigh on sentiment but Irish consumers still planning a reasonable if restrained Christmas spend.

November confidence reading buffeted by conflicting forces

Tech job losses prompt further significant downgrade of employment outlook …

…but household finances improve marginally, likely reflecting Budget boost

So pull-back in spending plans driven more by caution than by cash constraints

Overall, sentiment down only marginally, unlike corresponding US survey, suggesting Irish consumers are nervous but not despondent...

...So, survey suggests Consumer spending may slow but shouldn't slump

Special survey question finds only 5% of consumers have more spending power this Christmas than last year while 61% have less money for the festive season, a marked weakening compared to recent years

Roughly half of Irish consumers will fund Christmas spend from income, 1 in 3 consumers will use savings, while the remaining 1 in 5 will either borrow or don’t know how they will fund Christmas outlays

CONSUMER MINDSET REPORT

Read commentary and view charts related to this month’s Consumer Sentiment Index.

Contrasting influences translate into marginal drop in confidence in November

Irish consumer sentiment fell marginally in November as conflicting factors made for a more uncertain outlook. Budget support measures and comparatively favorable developments in the Irish economy combined with mild weather may have taken some of the immediate sting out of cost-of-living pressures. However, rapidly increasing concerns about job losses in the tech sector and a related caution about spending plans have proven slightly more influential drivers of consumer thinking of late. As a result, Irish consumer confidence was slightly lower in November than in October.

Contrasting movements in various elements of the survey suggest Irish consumers may feel they have braced themselves for a difficult winter ahead but, in a very uncertain world, consumers are constantly adjusting their sense of what may lie ahead and amending their spending plans accordingly.

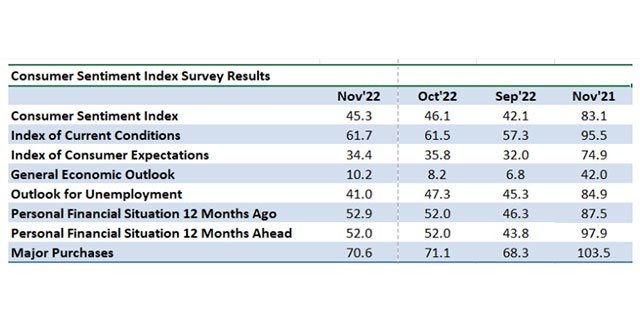

The Credit Union Consumer Sentiment Index edged down to 45.3 in November from 46.1 in October. The current reading suggests a very nervous Irish consumer but it is encouraging that it remains above the 14 year low of 42.1 seen in September. This suggests Budget support measures are having some positive impact as are less strained than feared energy markets globally. It might also be inferred from the November reading that Irish consumers feel they have prepared themselves as far as possible for a difficult winter ahead.

While sentiment can alter rapidly, an element of resilience in the Irish consumer sentiment reading for November is hinted at in a comparison with the closest comparable US measure which showed a significant and unexpected drop to a preliminary November reading of 54.7 from 59.9 in October (Note; it is more appropriate to look at changes in sentiment in the two countries rather than the absolute level of the two indices). The US measure showed a marked pullback in spending plans that might hint at a muted ‘Black Friday’ spend in the ‘States. A very negative-focussed election campaign coupled with major weakness in US technology and cryptocurrency stocks may have contributed to a notably gloomier mood among US consumers.

Perhaps surprisingly, Irish consumers were slightly less negative about the outlook for this economy in November. This may owe something to the resilience of most economic indicators and, possibly, the particular strength of tax revenues.

In part, modestly reduced ‘macro’ worries may also reflect several recent commentaries that suggested the Irish economy might avoid recession in the coming year. While this writer would suggest that too much attention is devoted to the somewhat arbitrary judgement as to whether changes in activity in aggregate are marginally positive or negative, Irish consumers are probably correct to judge that they may be spared the more extreme weakness likely to be seen in some of our economic neighbours. Moreover, the November reading suggests Irish consumers remain very downbeat about the broad economic environment even if a little less so than in October.

In spite of a little less gloom on the broad economic outlook, Irish consumers were notably more worried about job prospects. As income tax receipts remain healthy and unemployment data continue to track near historic lows, this significant downgrade of the employment outlook can be attributed to a flurry of layoff announcements in a number of tech companies through the survey period that raised broader concerns regarding the outlook for the tech sector as a whole.

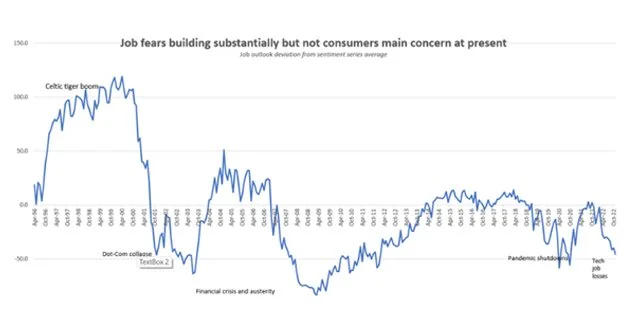

The graph below gives some sense of the extent of job worries on the part of Irish consumers at present. It shows the extent to which consumers rate job prospects over the following twelve months more or less favourably than the norm over the 26-year history of the sentiment survey.

As the graph suggests, a tendency towards sharp changes in Irish economic conditions has led to regular and substantial changes in consumer thinking on job prospects through the sentiment survey’s 26-year history.

The November ‘22 reading suggests that Irish consumers are currently quite gloomy about the outlook for employment but those concerns are not anywhere near as large as seen during the financial crisis when there was a sharp and sustained fall in numbers at work in the Irish economy. Neither are they quite as pronounced as those seen in the immediate wake of Covid-related lockdowns two years ago.

The degree of job worries now being signalled by the November consumer sentiment survey is much closer in scale to those seen in the wake of the Dot-Com collapse just over twenty years ago (when the jobless rate was similarly around 4%). Cost-of-living and economic slowdown concerns have been weighing on the outlook for jobs through much of 2022. However, the broader health of the Irish jobs market in recent years, coupled with widespread reports of significant unfilled vacancies and skill shortages in tech-related areas, appears to be producing a more measured if still material immediate reaction to the spate of job losses seen during the November survey period.

If the Credit Union Consumer Sentiment Index reading for November suggests no major spillover from tech job losses to other areas of the confidence survey, it is worth noting that the only other element to weaken this month was household spending plans. This hints that Irish consumers continue to adjust their outlays in the face of an increasingly uncertain environment.

Encouragingly, the pull-back in spending plans this month seems to owe more to imcreased caution rather than increasing cash constraints. The other personal finance elements of the November survey held up reasonably well. Consumers were a little less negative about their own current financial circumstances and the outlook for future finances was unchanged. So, Christmas spending seems likely to be careful rather than cancelled.

Irish consumer spending plans for Christmas 2022.

The Credit Union Consumer Sentiment survey for November contained a special question focussed on Irish consumers spending plans for Christmas 2022. This also allows a comparison with spending intentions for the previous two years when similar questions were asked.

It may be worth putting some context on the pressures Irish consumers now face. As noted previously, the marked pick-up in inflation in the past year represents a significant drain on Irish households spending power. With Irish inflation likely to be around 8% this year compared to 2.4% in 2021, consumers will find that their scope for discretionary spending at Christmas will be much reduced- on my rough calculations, higher inflation translates into a hit of about €3k to the average households buying power this year. Given that the approach of winter means much higher outlays on hugely more expensive heat and light as well as notably dearer grocery bills, the sense of ‘feel-poor’ is likely to be pronounced this Christmas.

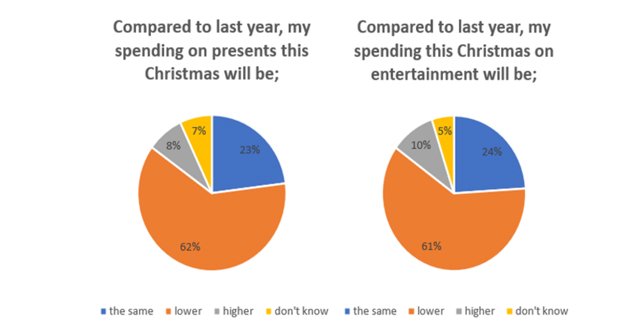

In these circumstances, it is scarcely surprising that most Irish consumers say they will have less to spend this Christmas than last. Only 5% of consumers say they will have more to spend this year than last year. As many as 61% consumers say they will have less to spend.

As the diagram below illustrates, this marks a substantial deterioration compared to last year’s results, when the cost of living was just beginning to accelerate notably, or the year before that, when Covid was affecting the income and outlays of many households.

While the decline in spending power is broadly based, slightly fewer under 25’s and over 65’s, slightly ferwer Dublin-based consumers and significantly fewer consumers on higher incomes say they have less to spend than last year.

We also asked consumers to indicate whether they would spend more or less on gifts and entertainment this year. As the diagram below illustrates, the scale of planned increase or decrease in Christmas-related spending in these areas largely mirrors the expected increase or decrease in spending power.

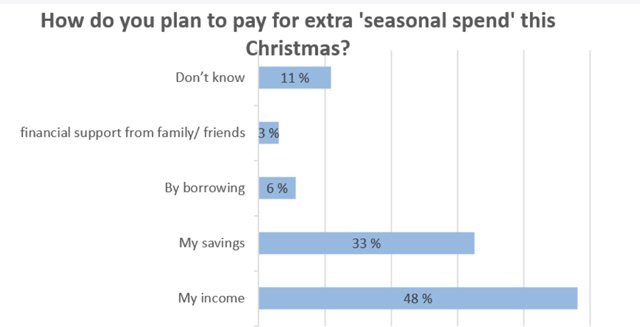

Finally, the November sentiment survey also included an additional question asking how consumers expected to finance Christmas-related spending. The results are shown in the diagram below. Roughly 1 in 2 consumers (48%) say that their spending will be funded from household income and a further 1 in 3 will use savings for their extra Christmas spending.

This means that about 1 in 5 consumers will either borrow to fund extra Christmas spending or don’t know how they will pay for it. ‘Don’t know’ responses were much more frequent among lower income households and those who say they were struggling to make ends meet. So, these responses seem to reflect financial strains rather than delayed decision making.

‘Don’t know’ responses tended to be more frequent among those aged below 45 whereas borrowing was most pronounced among those aged 45 to 54. It should also be noted that these responses are framed in the context of a very widespread cutback in planned Christmas spending. So, it appears that significant numbers will struggle to finance even a ’cut-back Christmas’ this year.

Although many if not most Irish households will be cautious in relation to their Christmas spend this year, across the economy as a whole, this doesn’t necessarily imply a frugal rather than festive season. Although spending power has been notably dented, numbers at work are set to be materially higher than a year ago, the population has increased significantly and Government financial supports are notably larger and now reaching most households.

In the same vein, the fact that the Credit Union Consumer Sentiment Index is holding steady, albeit at historically low levels and that the personal finance elements of the survey seem to have stabilised might suggest that while Irish consumer spending may be restrained it should still be reasonably healthy this Christmas.

The Irish Consumer Sentiment Survey is a monthly survey of a nationally representative sample of 1,000 adults. Since May 2019, Core Research have undertaken the survey administration and data collection for the Survey. The survey was live between the 3rd – 15th November 2022.